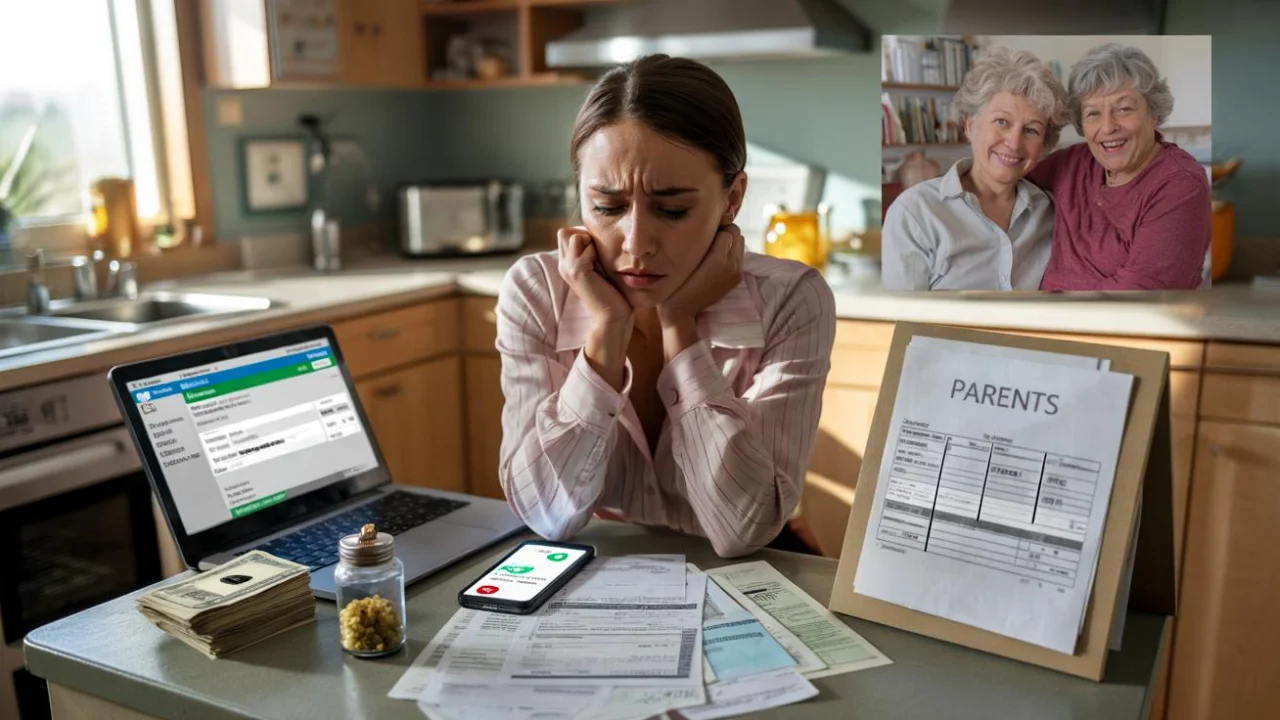

Sarah gets paid every two weeks on Thursday. By Friday morning, she’s already transferred $400 to her mom’s account for groceries and utilities. By the weekend, another $200 disappears when her dad calls about his car payment. She loves her parents deeply, but she’s 28 years old and still sleeping on a friend’s couch because she can’t save enough for a security deposit.

Sound familiar? Sarah’s story isn’t unique. Millions of adult children find themselves caught in an exhausting cycle of helping parents financially while their own dreams get pushed further away. The question that keeps many awake at night: when does family support cross the line into self-sacrifice?

The guilt feels crushing. These are the people who raised you, fed you, drove you to soccer practice. But what happens when helping parents financially starts destroying your own future?

When Family Support Becomes Financial Quicksand

There’s something nobody warns you about when you become the family’s unofficial ATM. It starts small—maybe $50 here and there for gas money or groceries. Then it grows. Suddenly, you’re covering rent, medical bills, car repairs, and credit card payments. Your parents’ financial emergencies become your monthly budget line item.

- Retirement trap when a beekeeper’s bees turn your peaceful plot into a taxable farm and the law says you owe even if you never saw a cent

- South Korea sparks fierce debate by unleashing long?range “submarine hunters” in contested waters, deepening regional tensions and testing how far a nation should go to secure its seas

- The uncomfortable truth about charitable donations: why your well?meant generosity might be propping up corruption, deepening inequality, and doing more harm than good

- Retirement betrayal: why lending land to a ‘friend’ beekeeper can cost you thousands in taxes and tear communities apart

- How a neighborly favor cost a retiree his peace: the beekeeper, the taxman, and the question tearing rural communities in two

- Why a retiree who lent land to a beekeeper must pay agricultural tax despite earning nothing and what this says about fairness, responsibility, and the quiet battles between neighborly goodwill and the taxman

Financial therapist Dr. Amanda Chen sees this pattern constantly in her practice. “Adult children often become financial enablers without realizing it,” she explains. “They think they’re being loving and responsible, but they’re actually preventing their parents from facing their financial reality.”

The numbers are staggering. Recent surveys show that 42% of millennials provide regular financial support to parents or older relatives. The average amount? Around $1,200 per month. That’s rent money, student loan payments, or retirement savings vanishing into someone else’s budget crisis.

Meanwhile, you’re living paycheck to paycheck, avoiding social events because you’re broke, and watching your credit score tank while your parents maintain their lifestyle. The resentment builds, but so does the guilt for feeling resentful.

The Real Cost of Playing Family Bank

Let’s break down what helping parents financially actually costs you beyond the monthly transfers:

| Hidden Cost | Long-term Impact |

|---|---|

| Delayed home ownership | Missing years of equity building |

| Reduced retirement savings | Working extra years before retirement |

| Emergency fund depletion | One crisis away from debt |

| Career limitations | Can’t take risks or lower-paying opportunities |

| Relationship strain | Arguments about money with partners |

| Mental health impact | Chronic stress and anxiety about finances |

Consider Marcus, a 35-year-old teacher who has been sending his parents $800 monthly for three years. That’s nearly $29,000 he could have invested. With compound interest, that money could have grown to over $65,000 by retirement age.

“I never thought about the opportunity cost,” Marcus admits. “I was so focused on helping them today that I forgot I need to help myself tomorrow.”

- Lost compound interest on savings and investments

- Delayed major life milestones like homeownership

- Increased stress affecting job performance and health

- Strained romantic relationships due to financial pressure

- Inability to build emergency funds for your own crises

Drawing the Line Without Destroying Family Bonds

Setting financial boundaries with parents feels like navigating a minefield. The manipulation can be subtle—tears, guilt trips, reminders of childhood sacrifices. But relationship counselor James Rodriguez argues that boundaries actually strengthen family relationships.

“When you enable financial dependency, you rob your parents of their dignity and agency,” Rodriguez notes. “True love sometimes means letting people face the consequences of their choices.”

Start with these practical steps:

- Calculate exactly how much you’ve been giving and what it’s costing your future

- Have an honest conversation about your own financial goals and limitations

- Offer specific types of help rather than open-ended cash transfers

- Set a firm monthly limit and stick to it, even if they ask for more

- Help them create a budget and explore other resources like government assistance

The conversation doesn’t have to be harsh. Try something like: “Mom, I love you and want to help, but I can only afford $200 per month going forward. Let’s figure out how to make that work for your most important expenses.”

Yes, there might be tears. There might be accusations of selfishness. But remember: you can’t pour from an empty cup. If you destroy your own financial future, you’ll eventually be unable to help anyone.

When Saying No Is Actually the Most Loving Thing

Financial advisor Lisa Park has seen too many clients sacrifice their own stability for parents who refuse to change their spending habits. “I’ve watched adult children go into debt to fund their parents’ lifestyle choices,” she says. “That’s not love—that’s codependency.”

Sometimes the kindest thing you can do is force your parents to confront their financial reality. This might mean:

- They have to downsize their housing

- They need to apply for government assistance programs

- They must sell unnecessary possessions or cars

- They have to take on part-time work if physically able

- They need professional financial counseling

It’s uncomfortable, but it’s reality. Your parents are adults who made financial decisions for decades. You shouldn’t have to sacrifice your own future because those decisions weren’t always wise.

Remember, helping parents financially should be a choice, not an obligation that destroys your own well-being. The goal is to build a sustainable support system that doesn’t require you to set yourself on fire to keep others warm.

FAQs

How much should I realistically help my parents each month?

Financial experts recommend no more than 10% of your after-tax income, and only after you’ve covered your own essentials and emergency savings.

Is it selfish to stop helping my parents financially?

No. Setting financial boundaries is healthy self-preservation, not selfishness. You can’t help anyone long-term if you destroy your own financial stability.

What if my parents threaten to cut contact if I stop helping?

This is emotional manipulation. Healthy relationships don’t depend on financial transactions. Consider family therapy to work through these dynamics.

How do I help my parents without giving them cash?

Pay specific bills directly, buy groceries, help them apply for assistance programs, or offer practical services like transportation to appointments.

What if my parents genuinely can’t survive without my help?

Research local resources like food banks, housing assistance, and senior services. Many communities have programs specifically designed to help older adults in financial distress.

Should I feel guilty about prioritizing my own financial future?

Absolutely not. Taking care of your own financial health ensures you’ll be able to help your family in genuine emergencies rather than chronic mismanagement.