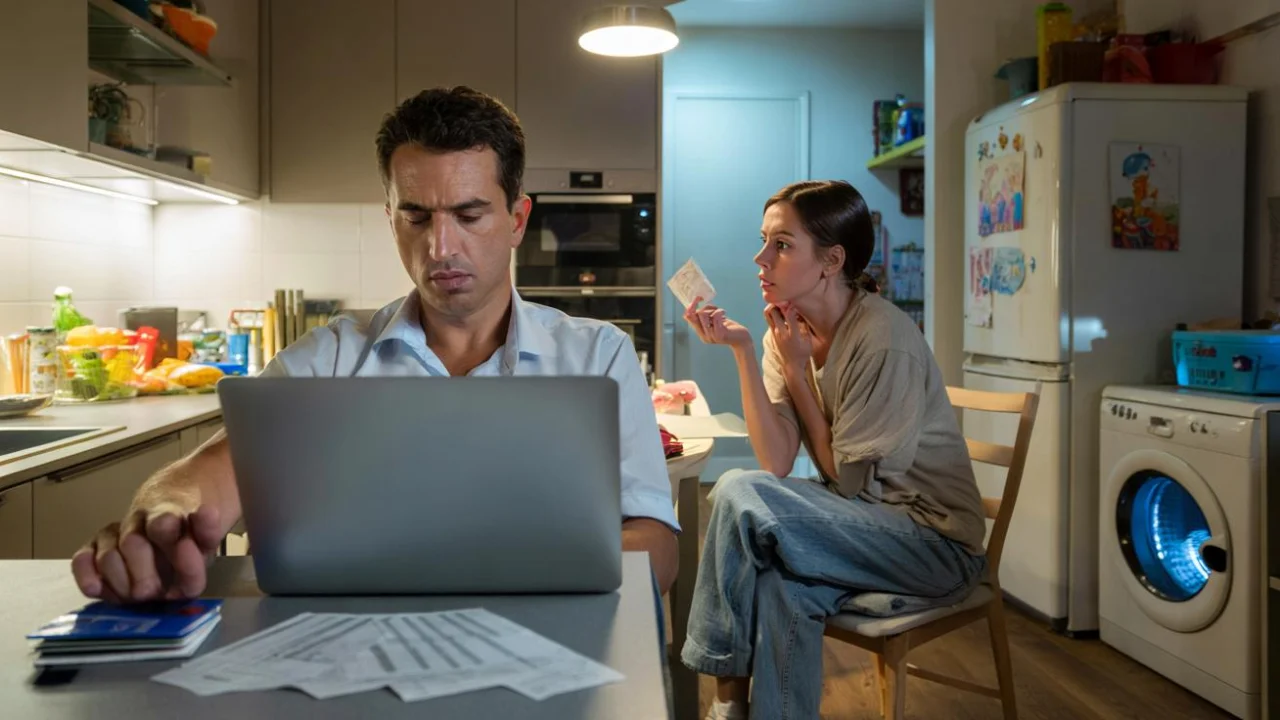

Sarah stares at the notification on her phone: “Transaction declined.” She’s standing in Target with her seven-year-old daughter, holding a $4 pack of colored pencils for a school project due tomorrow. Her husband controls their joint account, and she forgot to ask permission for this “unnecessary expense.”

Her daughter tugs at her sleeve. “Mommy, can we get them?” Sarah forces a smile and whispers they’ll come back later. But later means texting her husband, explaining why she needs money, and waiting for approval like a child asking for allowance.

This scene plays out in thousands of homes across America, where the line between financial responsibility and financial abuse has become dangerously blurred.

The Fine Line Between Thrift and Tyranny

Financial abuse affects approximately 1 in 4 women and 1 in 9 men, according to the National Network to End Domestic Violence. Yet it remains one of the most misunderstood forms of control because it often masquerades as fiscal responsibility.

- When ‘sensible’ becomes sabotage: how the one habit you proudly call prudence may be slowly killing your retirement dreams and exposing a generational lie about what “playing it safe” really costs

- When good deeds get taxed: A retiree who lent land for a young couple’s ‘dream’ tiny home is slapped with a huge property tax hike – officials insist it’s the law, neighbors say he’s gaming the system, and the whole town is torn over whether helping others should come with a financial punishment

- When a “harmless” favor becomes a legal nightmare: how a retiree’s kind gesture of lending land for a small apiary spiraled into an unexpected agricultural tax bill, a bitter clash with neighbors, and a fierce debate over whether the state is punishing community spirit or finally cracking down on hidden farm businesses

- When kindness backfires: how feeding stray cats can save lives, spread disease, poison neighborhoods, and spark a silent war between animal lovers and furious residents

- Injustice laid bare as a lifelong teetotaler loses custody of her children over a single drunken mistake: a necessary safeguard for vulnerable kids or a merciless system that brands parents forever, a story ripping public opinion in half

- Millions rejoice as coastal defenses rise, but inland farmers rage over new floodwall plan that sacrifices their crops to save seaside mansions

When Marc monitors every penny Anna spends, is he being a prudent provider or a controlling partner? The answer lies not in the spreadsheet, but in the power dynamics underneath it.

“True financial partnership involves shared decision-making and mutual respect,” explains Dr. Jennifer Wilson, a licensed therapist specializing in domestic abuse. “When one person unilaterally makes all money decisions and the other needs permission for basic purchases, that’s not budgeting—that’s control.”

The difference between healthy frugality and financial abuse often comes down to choice and autonomy. Couples who practice healthy money management discuss budgets together, set joint goals, and maintain individual freedom within agreed-upon boundaries.

Warning Signs That Frugality Has Become Financial Control

Financial abuse can be subtle, especially when disguised as concern for the family’s financial future. Here are the key red flags that distinguish controlling behavior from genuine fiscal responsibility:

- No access to accounts: One partner holds all passwords and account information

- Micromanaging small purchases: Requiring approval for basic necessities like groceries or personal care items

- Withholding information: Refusing to discuss income, savings, or major financial decisions

- Preventing employment: Sabotaging job interviews or demanding a partner quit work

- Hiding assets: Maintaining secret accounts or making large purchases without discussion

- Creating financial dependency: Ensuring the other partner has no money of their own

- Using money as punishment: Restricting access to funds after arguments or disagreements

“The key difference is consent and communication,” notes financial counselor Maria Rodriguez. “In healthy relationships, both partners have a voice in money decisions, even if one person handles the day-to-day management.”

| Healthy Financial Management | Financial Abuse |

|---|---|

| Both partners have account access | One partner controls all accounts |

| Budget discussions involve both people | One person sets all spending rules |

| Each person has some spending autonomy | All purchases require approval |

| Financial goals are set together | One partner makes unilateral decisions |

| Both partners can access emergency funds | Access to money is restricted or withheld |

The Psychological Impact of Money Control

The effects of financial abuse extend far beyond empty bank accounts. Victims often experience anxiety, depression, and a profound sense of helplessness that can persist long after the relationship ends.

Anna, whose story opened this piece, describes the constant mental calculations: “I’d stand in the grocery store doing math in my head, wondering if buying the name-brand cereal would trigger an interrogation later. Everything became about avoiding his disappointment.”

This hypervigilance around spending creates a state of chronic stress. Victims report feeling like children in their own homes, unable to make basic decisions about their daily lives.

“Financial abuse is particularly insidious because it attacks a person’s sense of independence and self-worth,” explains Dr. Susan Chen, who studies economic abuse patterns. “Money represents freedom and choice in our society. When someone controls your access to money, they’re controlling your ability to live autonomously.”

Breaking Free From Financial Control

Escaping financial abuse requires both emotional courage and practical planning. The first step is recognizing the behavior as abuse rather than excessive frugality or financial prudence.

Building financial independence starts small but requires secrecy and safety planning:

- Open a small savings account in your name only

- Keep cash hidden in a safe location

- Document financial abuse with screenshots and records

- Research local domestic violence resources

- Build credit in your own name if possible

- Identify supportive friends or family members

Many financial institutions now offer programs specifically designed to help abuse victims establish independent banking relationships safely and discreetly.

“The most dangerous time is often when someone decides to leave,” warns domestic violence advocate Rachel Torres. “Financial abusers may escalate their behavior when they sense they’re losing control.”

When “Providing” Becomes “Controlling”

Society often celebrates the breadwinner who “handles the finances” and “protects the family’s money.” This cultural narrative can make it difficult for both victims and observers to recognize when provision becomes oppression.

Marc genuinely believed he was being a responsible husband by monitoring every expense. In his mind, tracking Anna’s spending protected their children’s future and demonstrated his commitment to their family’s security.

But Anna’s experience tells a different story. She describes feeling “erased” from her own life, unable to buy her daughter a book or grab lunch with colleagues without explanation and justification.

“Intent doesn’t erase impact,” Dr. Wilson emphasizes. “Many financial abusers genuinely believe they’re being helpful or protective. But the result is the same: one partner loses their autonomy and dignity.”

FAQs

How can I tell if my partner’s money management is abusive or just strict?

Ask yourself if you have any say in financial decisions and whether you can access money for basic needs without permission. Healthy budgeting involves both partners; financial abuse involves one person controlling everything.

Is it financial abuse if my spouse makes more money and wants to control spending?

Yes, the income difference doesn’t justify complete financial control. Even if one partner earns less or stays home, both deserve access to household funds and input on spending decisions.

What should I do if I suspect a friend is experiencing financial abuse?

Listen without judgment and avoid telling them what to do. Share resources about financial abuse and let them know you’re available for support when they’re ready to seek help.

Can financial abuse happen to men too?

Absolutely. While women are more commonly victims, financial abuse affects people of all genders. Men may face additional barriers to seeking help due to social stigma.

How do I rebuild my finances after leaving a financially abusive relationship?

Start with basic banking and credit-building. Many organizations offer financial literacy programs specifically for abuse survivors. Consider working with a financial counselor who understands domestic violence dynamics.

Where can I get help if I’m experiencing financial abuse?

Contact the National Domestic Violence Hotline at 1-800-799-7233. They can connect you with local resources and safety planning assistance. Many communities also have financial empowerment programs for abuse survivors.