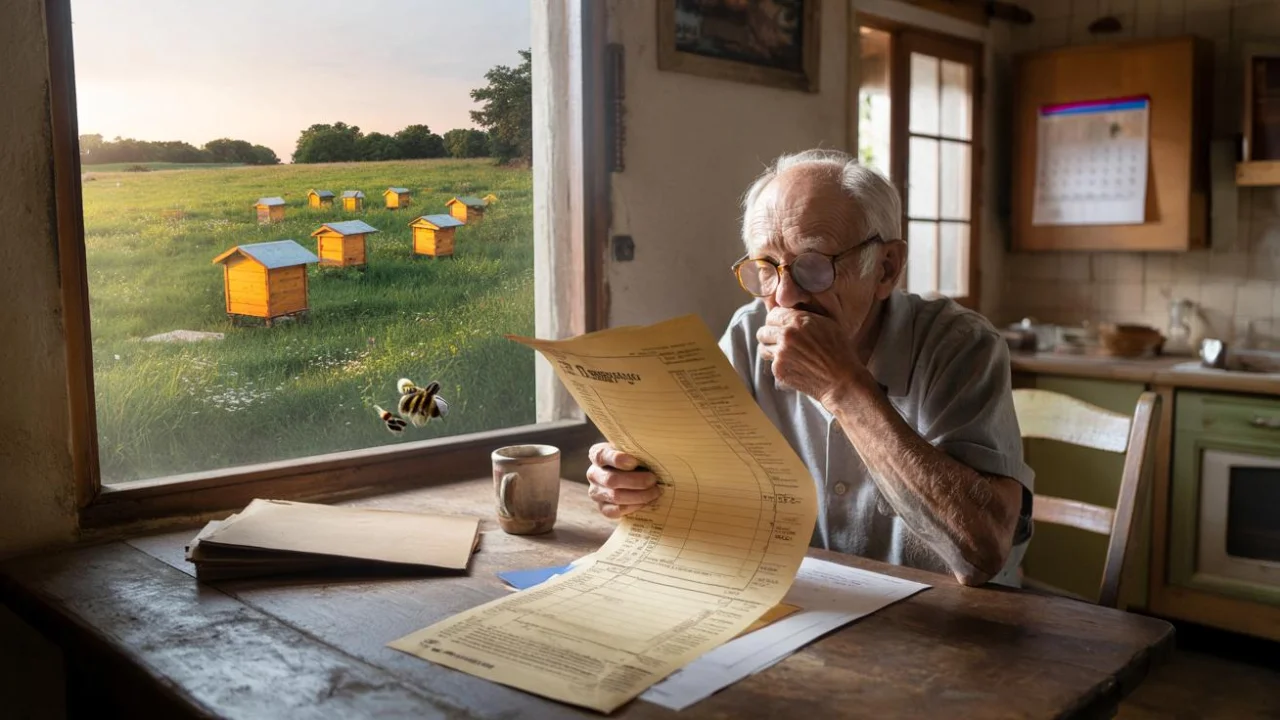

Jacques never imagined that helping a neighbor could cost him thousands. The 68-year-old retiree was enjoying his morning coffee when he spotted the young beekeeper walking up his driveway, hat in hand and worry lines creasing his forehead. “I need a safe place for my hives,” the man explained, “somewhere away from the pesticides.” Jacques looked out at his unused corner of land, overgrown with wildflowers, and shrugged. “Sure, why not?”

No paperwork. No rental agreement. Just a handshake between neighbors and the promise of a few jars of honey come Christmas. Twelve months later, Jacques received an agricultural tax bill that made his pension look like pocket change. What started as a simple favor had somehow transformed his property into a commercial agricultural operation in the eyes of the tax office.

Now Jacques faces a financial nightmare that’s splitting public opinion across the country. Is this bureaucratic overreach, or simply the law working as intended?

When Good Neighbors Meet Bad Tax Laws

Jacques’s story isn’t unique. Across rural communities, similar scenarios play out when informal agreements collide with rigid tax classifications. The moment those wooden hives appeared on his land, satellite imagery and routine administrative checks flagged his property for reclassification.

- Retirement ruined or tax justice served as a landowner who lent fields to a beekeeper is ordered to pay agricultural levies despite claiming he earned nothing, igniting a bitter nationwide debate over whether goodwill should be punished or profitable loopholes finally closed

- Scientists create synthetic womb capable of growing human embryos to term, and the world must now decide if this is progress or pure madness

- How a neighborhood feud over a homemade treehouse ended with a court order, a family divided, and a community asking if safety rules have gone too far

- Everyone loves cheap flights until they learn what they really cost the people living under the flight paths

- Sleepless investors facing an uneasy choice: should they bet their life savings on a tech giant whose AI might one day make their own children unemployed? A dilemma tearing families, experts and entire economies apart

- Longevity lies: A man who chose eternal life over his family returns 50 years later, still young, to demand his inheritance from his own grandchildren

“The tax office doesn’t care about handshakes and good intentions,” explains Marie Dubois, a rural property tax consultant. “They see productive agricultural activity on a piece of land, and someone has to pay the corresponding taxes.”

The reclassification triggered backdated agricultural tax obligations stretching over the entire period the hives were present. For Jacques, this meant a bill equivalent to several months of his modest retirement income. Meanwhile, the actual beekeeper—the one generating income from the honey—faced no additional tax burden whatsoever.

The legal reasoning is straightforward: landowners are responsible for tax obligations related to activities on their property, regardless of who benefits financially. But this creates a perverse situation where the person lending the land pays more than the person profiting from it.

The Hidden Costs of Agricultural Tax Reclassification

Understanding how a simple favor can trigger an agricultural tax bill requires looking at the complex web of land use classifications and tax obligations. Here are the key factors that turned Jacques’s goodwill gesture into a financial burden:

- Automatic reclassification: Any commercial agricultural activity on land triggers immediate tax category changes

- Retroactive billing: Tax obligations apply from the moment activity begins, not when discovered

- Owner liability: Property owners bear full tax responsibility regardless of who profits

- No minimum threshold: Even small-scale activities like a few beehives can trigger reclassification

- Satellite monitoring: Advanced imagery makes it nearly impossible to avoid detection

The financial impact varies significantly depending on location and property size, but the pattern remains consistent across different regions:

| Property Type | Average Annual Increase | Retroactive Penalty Range |

|---|---|---|

| Small rural plots (under 2 acres) | €800-1,500 | €2,000-4,000 |

| Medium properties (2-5 acres) | €1,500-3,000 | €4,000-8,000 |

| Large holdings (over 5 acres) | €3,000+ | €8,000+ |

“What we’re seeing is a fundamental disconnect between how rural communities operate and how tax law functions,” notes Pierre Martineau, a rural affairs advocate. “Neighbors help neighbors—it’s been that way for generations. But the tax system doesn’t recognize informal arrangements.”

A Nation Divided Over Fairness

Jacques’s case has sparked heated debate about the fairness of current agricultural tax policies. Supporters argue that tax laws must be applied consistently to prevent abuse and ensure proper revenue collection. Critics contend that penalizing acts of neighborly kindness represents bureaucracy at its worst.

Rural communities have rallied around cases like Jacques’s, organizing petition drives and social media campaigns. Urban taxpayers, however, often view these situations differently, arguing that property owners should understand their tax obligations before allowing commercial activities on their land.

“This isn’t just about one retiree and some beehives,” explains Agricultural Policy Institute researcher Dr. Sarah Blackwood. “It’s about whether our tax system can adapt to modern rural realities or if it will continue punishing informal cooperation.”

The ripple effects extend beyond individual property owners. Beekeepers now struggle to find suitable locations for their hives, as potential hosts fear unexpected tax consequences. Environmental groups worry that stricter enforcement could harm pollinator conservation efforts that depend on these informal arrangements.

Some regions have begun exploring policy modifications to address these concerns. Proposed solutions include minimum revenue thresholds before tax reclassification kicks in, exemptions for environmental activities, and formal recognition of “courtesy arrangements” that don’t trigger commercial tax obligations.

Legal Loopholes and Practical Solutions

For property owners currently facing similar situations, several strategies might help minimize agricultural tax bill impacts:

- Document the arrangement: Written agreements clarifying that no rent is charged can sometimes help

- Limit duration: Temporary arrangements may receive different treatment than permanent installations

- Appeal classifications: Tax offices sometimes reverse decisions when presented with proper documentation

- Seek legal counsel: Experienced rural property lawyers often find overlooked exemptions

Jacques is currently working with a legal aid organization to challenge his agricultural tax bill. His lawyer believes the case has merit because no formal commercial relationship existed between Jacques and the beekeeper.

“The law needs to distinguish between genuine commercial agricultural activities and neighborly favors,” argues his attorney, Claire Rousseau. “Otherwise, we’re going to see rural communities become increasingly isolated and less cooperative.”

The case has attracted national attention, with agricultural policy experts watching closely to see how courts interpret these informal arrangements. The outcome could influence how thousands of similar cases are handled nationwide.

FAQs

Can I let someone use my land for farming without facing tax consequences?

Unfortunately, any commercial agricultural activity on your property can trigger tax reclassification, even if you don’t receive payment.

How do tax offices discover these arrangements?

Satellite imagery monitoring and cross-referencing with local business registrations help identify undeclared agricultural activities.

What’s the difference between helping a neighbor and commercial agriculture?

Tax law focuses on the activity itself, not the financial arrangement, so even free use can be considered commercial if productive work occurs.

Are there any exemptions for environmental activities like beekeeping?

Currently, most tax systems don’t distinguish between different types of agricultural activities when determining tax obligations.

Can I appeal an agricultural tax reclassification?

Yes, most jurisdictions allow appeals, though success depends on specific circumstances and local regulations.

Should I get a lawyer if I receive an unexpected agricultural tax bill?

Given the complexity of land use law and potential for significant financial impact, legal consultation is often worthwhile for substantial bills.