Sarah stared at her grocery receipt, watching the numbers blur as tears welled up in her eyes. Another month, another $700 shortfall. She’d done everything right – tracked expenses, avoided impulse purchases, even skipped her morning coffee runs. Yet here she was again, standing in her kitchen with half the groceries she needed and a bank account that seemed to hemorrhage money despite her best efforts.

The breaking point came when she realized she wasn’t financially irresponsible. She was just planning at the wrong times. What seemed like a massive budget gap fix turned out to be surprisingly simple – it wasn’t about spending less, but about timing her planning differently.

Like millions of Americans living paycheck to paycheck, Sarah discovered that the traditional monthly budgeting approach was sabotaging her financial stability in ways she never imagined.

The Hidden Problem with Monthly Budget Planning

Most people budget the way they were taught – by calendar months. January 1st to January 31st, neat and tidy. But here’s the problem: your bills don’t care about calendar months, and neither does your paycheck schedule.

- This one shampoo trick slowly darkens grey hair without anyone knowing you’re doing it

- The longest total solar eclipse in 100 years will plunge day into eerie darkness for millions this week

- This $200 device masters 9 cooking methods while your air fryer collects dust

- This sleek air fryer replacement is quietly making microwaves obsolete in kitchens across America

- Why every fresh haircut transformation actually peaks 3 weeks later, not on day one

- Scientists stunned as comet 3I Atlas reveals we might be missing dangerous visitors from deep space

Sarah’s revelation came during a Sunday afternoon spent analyzing her spending patterns. She discovered that her $700 budget gap wasn’t caused by overspending on luxuries or poor financial discipline. The culprit was a fundamental mismatch between when she planned her money and when she actually received it.

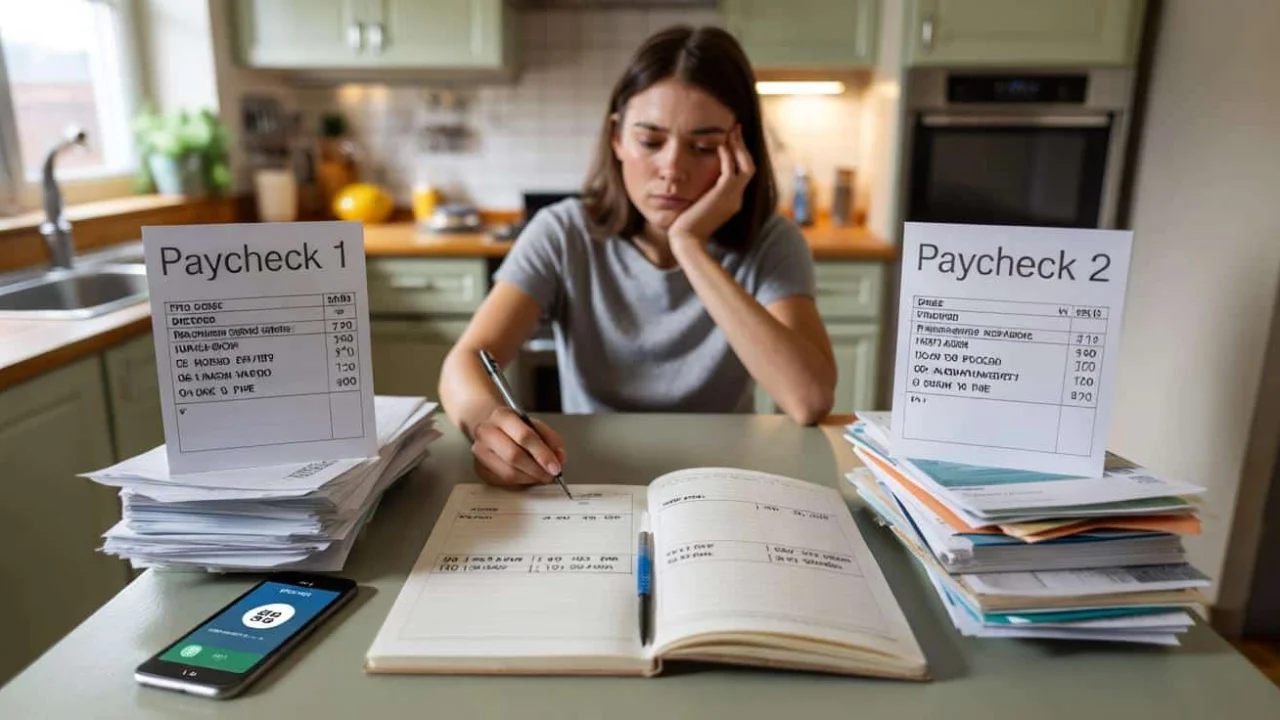

“I was getting paid on the 1st and 15th, but my rent hit on the 5th, car payment on the 17th, and insurance on the 28th,” Sarah explains. “My bills were scattered across the month like confetti, but I kept trying to make them fit into a monthly box.”

The result? One paycheck would be responsible for nearly three weeks of expenses, while the other barely lasted two weeks. This created a cascading effect where she’d feel financially secure right after payday, then gradually panic as bills accumulated faster than her planning had anticipated.

Breaking Down the Pay-Period Budget Method

The solution that eliminated Sarah’s budget gap was deceptively simple: plan by pay periods, not calendar months. Here’s how this approach works in practice:

| Traditional Monthly Budget | Pay-Period Budget |

|---|---|

| Plans January 1-31 | Plans Paycheck 1: 1st-14th, Paycheck 2: 15th-31st |

| Assigns all monthly income to cover all monthly expenses | Assigns each paycheck to cover specific bills in that period |

| Creates false sense of monthly abundance | Shows real-time cash flow limitations |

| Bills hit randomly throughout month | Bills are strategically assigned to appropriate paycheck |

Financial advisor Maria Rodriguez notes, “When clients switch to pay-period budgeting, they immediately see why they’ve been struggling. It’s not about income – it’s about cash flow timing.”

The key steps for implementing this budget gap fix include:

- List your exact pay dates for the next three months

- Identify which bills fall between each pay period

- Assign fixed expenses to the paycheck that can best handle them

- Split variable expenses like groceries and gas between both paychecks

- Move bill due dates if possible to balance the load

Why This Simple Change Creates Immediate Results

The beauty of pay-period budgeting lies in its brutal honesty. When Sarah divided her expenses this way, she immediately saw that her first paycheck was trying to cover $2,100 in expenses with only $1,800 in income. No wonder she was always short.

“The math became impossible to ignore,” Sarah recalls. “I couldn’t pretend that somehow magically the money would stretch. I had to make real decisions about what each paycheck could actually handle.”

This approach forces you to confront reality in ways monthly budgeting doesn’t. You can’t rely on “future money” to cover current expenses because you’re only planning 14 days ahead at most.

Personal finance expert David Chen explains, “Monthly budgets create an illusion of abundance because you’re looking at your total monthly income. Pay-period budgets show you the reality of what each individual paycheck can accomplish.”

Within two months of switching to this system, Sarah had eliminated her $700 budget gap. She moved her car payment to align with her second paycheck, shifted some subscriptions to spread the load more evenly, and most importantly, stopped mentally “borrowing” from future paychecks.

Making the Switch Without Disrupting Your Life

Transitioning to pay-period budgeting doesn’t require a complete financial overhaul. Start by tracking your current pay schedule and bill due dates for one month. Most people discover they can solve 80% of their timing issues by moving just 2-3 bill due dates.

The psychological impact is immediate. Instead of feeling broke by mid-month, you’ll know exactly what each paycheck needs to accomplish. This eliminates the anxiety of wondering where your money went and replaces it with clear, actionable planning.

Budget counselor Jennifer Walsh observes, “Clients who make this switch report feeling more in control within weeks. They’re not smarter with money – they’re just working with their actual cash flow instead of against it.”

For people paid weekly or every two weeks, this method becomes even more powerful. You can align your planning exactly with your income, creating a sustainable rhythm that doesn’t require superhuman discipline or deprivation.

FAQs

How long does it take to see results from pay-period budgeting?

Most people notice improved cash flow within 2-4 weeks, with the full budget gap fix typically achieved within 2-3 months.

What if my bills are due at inconvenient times?

Contact your creditors to move due dates. Most companies allow you to change due dates once or twice per year without penalties.

Does this work if I’m paid irregularly?

Yes, but you’ll need to estimate conservatively and plan for your lowest typical pay period rather than your highest.

Can I still save money with this method?

Absolutely. Assign savings as a “bill” to whichever paycheck can best handle it, just like any other expense.

What’s the biggest mistake people make when switching?

Trying to change everything at once. Start by just tracking your current patterns for one month before making major adjustments.

Will this work for irregular expenses like car repairs?

Build a small emergency buffer into each paycheck period. Even $25-50 per paycheck creates a meaningful cushion over time.